Small Business Life Insurance

Protect your business, your partners, and your employees with comprehensive life insurance solutions tailored for small businesses.

Why Your Business Needs Life Insurance

As a small business owner, you've invested countless hours and resources into building your company. Life insurance isn't just about protecting your family—it's about ensuring business continuity, protecting your partners, and providing security for your employees.

Key Benefits for Small Businesses

- Business Continuity: Ensure your business can continue operating even if a key person passes away

- Buy-Sell Agreements: Fund agreements that allow surviving partners to buy out a deceased partner's share

- Key Person Insurance: Protect against the financial impact of losing critical employees or executives

- Employee Benefits: Attract and retain top talent by offering life insurance as part of your benefits package

- Debt Protection: Cover business loans and debts to prevent burden on surviving partners or family

Types of Business Life Insurance

Key Person Insurance

Most businesses have owners, executives, or officers that play a key role in the success, sustainability, and profitability of the company. Should a key person die, you immediately lose all the skills and talents that were so vital to the company. Even for small business owners, life insurance will help you recover quickly.

The company can buy and own a life insurance policy for everyone deemed a key person. The company pays the premiums and as the beneficiary, receives the tax-free death benefit should a key employee die. This cash benefit can help offset lost sales and earnings, but more importantly, allow the company to quickly find and train a proper replacement.

Four Key Benefits of Key Person Life Insurance

Maintain Revenue

When the person who is missing is a big contributor to sales and/or cash flow, the key person insurance will help ensure sufficient funds are available until revenue can be replaced. Creditors and suppliers have businesses to run and cannot afford to miss out on payment.

Protect Your Assets

Companies often have mortgages on real estate and obligations to pay. The person who is missing is often a key person responsible for sales and revenue. Key person insurance shows lenders you have foresight for this kind of situation.

Cash Flow

If there is an interruption to the flow of funds due to the loss of a key person, it can result in a loss of market shares, a decline in sales, and an unexpected loss. The proceeds from the insurance can help fill the gap.

Protect Existing Equity Owners

Oftentimes, the key person is also an owner of the business, and their family will inherit his or her business assets. Insurance owned by the company can help to pay business obligations to the family.

Buy-Sell Agreement Funding

Life insurance provides the funds needed for surviving business partners to purchase a deceased partner's share of the business, ensuring smooth ownership transition and fair compensation for the deceased's family.

Learn More About Buy-Sell Agreement Funding

When an owner or partner in a business passes away, the business must quickly shift into survival mode and adapt effectively, or the company itself may face serious challenges. A buy-sell agreement funded by life insurance can safeguard you and your company from unexpected or unintended ownership transfers.

The sale and purchase of company shares are typically triggered by specific events such as death, disability, or retirement. The agreement clearly defines who can buy, who must sell, when transfers occur, and at what price.

There are permanent life insurance policies which have higher premiums than term-limited coverage, but offer long-term benefits. Because business valuations and financial needs can increase over time, consider policies that offer inflation protection. An experienced insurance advisor can be invaluable in structuring such a plan.

Are you a business owner? Here are 5 key reasons why you should have a buy-sell agreement in place:

Control

Do you have the peace of mind knowing you've put the right safeguards in place to ensure your business's success after you're gone? With a buy-sell agreement, you gain that crucial peace of mind.

Guaranteed Buyer

Through advance planning, you'll have certainty that a buyer is already identified and funding is secured, eliminating uncertainty during difficult times.

Predetermined Price

Establishing a predetermined price eliminates the stress and conflict that often arises from valuation negotiations during emotional times.

Tax Relief

When the death benefit equals the value of the deceased's business share, there is no taxable gain for federal income tax purposes. Additionally, if certain requirements are met, the predetermined price in the buy-sell agreement establishes the business value for federal estate tax purposes.

Treat Non-Business Family Members Fairly

Planning ahead ensures your family receives fair compensation and isn't placed in difficult or compromising positions regarding business decisions they may not be equipped to handle.

How Buy-Sell Agreements Work

Group Term Life Insurance

Offer life insurance coverage to your employees as part of their benefits package. This helps attract and retain quality employees while providing them with valuable protection for their families.

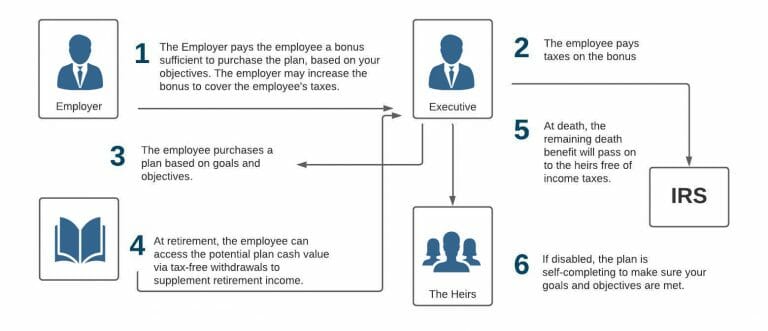

Executive Bonus Plans

Sometimes referred to as a Section 162 plan, an Executive Bonus Plan is a non-qualified executive insurance plan used by an employer to provide extra compensation to key executives. The business pays a tax-deductible bonus which the employee uses to pay the premiums for a personally owned life insurance policy.

This bonus is taxable income to the employee. The employee may have access to policy cash values and ultimately the beneficiary designated by the employee will receive the tax-free death proceeds.

Considering an Executive Bonus Plan? Here are some Key Tips!

Executive Bonus Plan – Pros for the Employer:

- •The plan provides the executive with post-retirement benefits. The life insurance policy stays in force and access to cash value after the executive has retired or left the company.

- •Unlike other non-qualified plans, the employer's premium payments are tax-deductible as compensation.

- •Plans are easy to administer as premiums are paid as salary payments for accounting purposes. In addition, there are typically no government reporting or disclosure requirements with which the plan must comply.

Executive Bonus Plan – Pros for the Executive:

- •The executive life insurance plan provides the executive with post-retirement benefits. The executive insurance policy stays in force and access to cash value after the executive has retired or left the company.

- •The plan is portable for the executive. Although the company will cease to make payments at the separation of employment, the executive may elect to continue the plan.

- •The executive uses company funds to pay for personal life insurance that will benefit his/her family in the case of unplanned loss of life.

Executive Bonus Plan – Cons for the Employer:

- •Since the executive owns the plan the employer has no control over the policy or its values.

- •Inability to recover any cost associated with the plan when the employee leaves.

Executive Bonus Plan – Cons for the Employees:

- •The amount bonused into the plan is considered income. However, many plans will also pay the taxes deeming the plan as a double-bonus executive bonus plan, thus eliminating this disadvantage.

Flow Chart of a Section 162 Restricted Executive Bonus Plan

- • Specific number of years, OR

- • Retirement age reached, OR

- • Other agreed events

- • Tax-free proceeds

- • Paid to executive's designated beneficiary

- • No waiting period

Key Points About Restrictions:

- •Executives may access policy cash values only after a certain number of years has passed or a specific event has occurred (such as attaining normal retirement age) as provided in the restricted bonus agreement between the parties.

- •There is no restriction on payment of death proceeds to the Executive's beneficiaries.

Getting Started

Every business is unique, and so are its insurance needs. Our experienced advisors will work with you to understand your business structure, financial goals, and succession plans to design a customized life insurance solution that protects what you've built.

Whether you're a sole proprietor, partnership, LLC, or corporation, we have solutions that fit your business model and budget. Let us help you secure your business's future and provide peace of mind for you, your partners, and your employees.

Ready to Protect Your Business?

Schedule a free consultation with one of our business insurance specialists today.

Schedule Your Free Consultation

Get expert advice tailored to your financial goals. No obligation, no pressure.